You get what you pay for. Or do you?

Newspaper companies are emphasizing profits instead of investing in the future of their embattled franchises, because their top executives are being paid to maximize near-term earnings at the expense of the long-term health of their companies.

It is perfectly reasonable to encourage executives of a robust and growing industry to maximize profit growth, so as to increase stock prices for the shareholders to whom they ultimately answer. But this is a dangerously bad idea for newspaper companies, which, as discussed at length here and elsewhere, are losing credibility, circulation and advertising market share all at the same time.

So long as newspaper executives are paid to prioritize bottom-line growth, they will continue to focus on profitability, instead of building new audiences and developing the fresh, sustainable revenue opportunities that will ensure the long-term health of their enterprises.

In the absence of the healthy sales gains the industry lately has not been able achieve, the only way to build profits is by cutting spending. Thus, newsroom staffing has dropped 4% since 2001 and publishers reportedly are trimming -- rather than expanding -- their investments in the new media that could strengthen their weakening market positions.

Even though most newspaper executives know they should be investing more, not less, in their businesses, they are trapped by a compensation system that explicitly forces them to manage their companies to please the stock market, which prizes steady, predictable gains in profits. A Gannett filing to the Securities and Exchange Commission exemplifies the language typically employed by the other public newspaper companies:

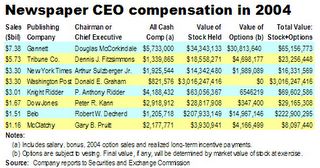

The average pay last year was more than $2.5 million among the chief executives of the eight publicly held newspaper companies with $1 billion or more in annual sales, according our survey of the proxy statement filed by each company with the SEC.

The largest paycheck, $5.7 million, went to Mr. McCorkindale, whose company was by far the biggest with $7.38 billion in revenues in 2004. The smallest paycheck, $821,576, went to Donald E. Graham of the Washington Post, who can console himself with interests in more than $3 billion of stock in his family company. (Full details are in the table below.)

Although a publishing CEO's multimillion-dollar pay package is considerably higher than Newspaper Guild scale, it is well within the norm for the chief of a large U.S. corporation. And it's downright puny when compared with the collective $160 million hauled out of Viacom last year by CEO Sumner Redstone and his two top lieutenants.

As is the case in nearly every industry, the CEO's cash comp is only a fraction of his or her over-all compensation. The really big money is in the amount of stock and stock options an executive can accumulate during his time at a company.

A word on options: Options enable an executive to buy shares of his company at a discount after a certain period of time. If the stock fails to rise enough during the prescribed period, the options may become worthless. If the stock price rises higher than the cost of the option, then the options are deemed to be "in-the-money." The table below includes the estimated value of in-the-money options as reported by the companies. Between now and the time the options are exercised, the value of those options could change -- and even evaporate.

Apart from Mr. Graham, the biggest accumulation of stock and options among the eight CEOs is held by Robert W. Dercherd of Belo, who owns nearly $223 million in his company's securities, based on the value of Belo's stock on April 18, 2005. The smallest portfolio, $8 million, belongs to Gary Pruitt of McClatchy Newspapers, who, ironically, is the only CEO in the group whose company's value is higher today than it was on Dec. 1, 2004.

Despite the aggregate $20.4 million in cash compensation and the more than $3.7 billion in securities in the hands of the eight CEOs, the stock of only two of their companies increased materially in value in 2004. Stock of the closely held Washington Post rose 24.21% last year and McClatchy gained 4.38%. The shares of all the other companies fell in 2004, trailing both the Standard & Poor 500 and the collective performance of all the shares in the media group. (Other gauges of performance are detailed in the following post.)

After the stock market was hammered broadly last week, only one newspaper stock, McClatchy, is still worth more today than in January, 2004. Newspaper stocks "had their worst week in memory, despite already low expectations going into the week," said securities analyst John Janedis of Banc of America Securities, adding that missed 2004 sales targets "offset by cost controls were not enough to satisfy [market] concerns of another disappointing year [in 2005]."

So, not only are credibility, circulation and market share crumbling, but stock prices are falling, too. Why?

The market moves for many mysterious reasons, but this one is obvious: Investors, who generally like to bet on the long-term upside of a company, are worried that the publishers don't have a plan for the future of the newspaper business.

While existing shareholders for the moment may be comfortable harvesting the properties for profits, there is not enough new money confident in the long-term prospects for newspapers to lift the value of their stocks.

If newspaper investors want their shares to rise significantly in the future, they are going to have to encourage management to emphasize top-line, not bottom-line, growth. If they don't, they some day will wake up to find the news business has gone the way of the once indomitable Penn Central Railroad.

To change management behavior, the incentives offered to newspaper executives have to reward the development of new products that leverage the existing strengths of their franchises to create sustainable and growing revenues from both existing and new audiences.

Opportunities abound in everything from direct-marketing programs to cellphone text messanging and from targeted, free print editions to paid, premium online content. But newspaper companies won't explore these and many other potentially lucrative paths unless their executives know they can venture outside the box without getting their ears boxed.

The current compensation system not only doesn't encourage change. It all but prohibits it.

It is perfectly reasonable to encourage executives of a robust and growing industry to maximize profit growth, so as to increase stock prices for the shareholders to whom they ultimately answer. But this is a dangerously bad idea for newspaper companies, which, as discussed at length here and elsewhere, are losing credibility, circulation and advertising market share all at the same time.

So long as newspaper executives are paid to prioritize bottom-line growth, they will continue to focus on profitability, instead of building new audiences and developing the fresh, sustainable revenue opportunities that will ensure the long-term health of their enterprises.

In the absence of the healthy sales gains the industry lately has not been able achieve, the only way to build profits is by cutting spending. Thus, newsroom staffing has dropped 4% since 2001 and publishers reportedly are trimming -- rather than expanding -- their investments in the new media that could strengthen their weakening market positions.

Even though most newspaper executives know they should be investing more, not less, in their businesses, they are trapped by a compensation system that explicitly forces them to manage their companies to please the stock market, which prizes steady, predictable gains in profits. A Gannett filing to the Securities and Exchange Commission exemplifies the language typically employed by the other public newspaper companies:

The award of these stock options continues to be an effective way of aligning [Chief Executive Officer Douglas] McCorkindale's financial interests to those of the company's other shareholders, because the value of these stock options is directly linked to increases in shareholder value.Given the size of their compensation packages and their presumed desire to ensure their future job security, you can't blame newspaper CEOs for playing by the rules.

The average pay last year was more than $2.5 million among the chief executives of the eight publicly held newspaper companies with $1 billion or more in annual sales, according our survey of the proxy statement filed by each company with the SEC.

The largest paycheck, $5.7 million, went to Mr. McCorkindale, whose company was by far the biggest with $7.38 billion in revenues in 2004. The smallest paycheck, $821,576, went to Donald E. Graham of the Washington Post, who can console himself with interests in more than $3 billion of stock in his family company. (Full details are in the table below.)

Although a publishing CEO's multimillion-dollar pay package is considerably higher than Newspaper Guild scale, it is well within the norm for the chief of a large U.S. corporation. And it's downright puny when compared with the collective $160 million hauled out of Viacom last year by CEO Sumner Redstone and his two top lieutenants.

As is the case in nearly every industry, the CEO's cash comp is only a fraction of his or her over-all compensation. The really big money is in the amount of stock and stock options an executive can accumulate during his time at a company.

A word on options: Options enable an executive to buy shares of his company at a discount after a certain period of time. If the stock fails to rise enough during the prescribed period, the options may become worthless. If the stock price rises higher than the cost of the option, then the options are deemed to be "in-the-money." The table below includes the estimated value of in-the-money options as reported by the companies. Between now and the time the options are exercised, the value of those options could change -- and even evaporate.

Apart from Mr. Graham, the biggest accumulation of stock and options among the eight CEOs is held by Robert W. Dercherd of Belo, who owns nearly $223 million in his company's securities, based on the value of Belo's stock on April 18, 2005. The smallest portfolio, $8 million, belongs to Gary Pruitt of McClatchy Newspapers, who, ironically, is the only CEO in the group whose company's value is higher today than it was on Dec. 1, 2004.

Despite the aggregate $20.4 million in cash compensation and the more than $3.7 billion in securities in the hands of the eight CEOs, the stock of only two of their companies increased materially in value in 2004. Stock of the closely held Washington Post rose 24.21% last year and McClatchy gained 4.38%. The shares of all the other companies fell in 2004, trailing both the Standard & Poor 500 and the collective performance of all the shares in the media group. (Other gauges of performance are detailed in the following post.)

After the stock market was hammered broadly last week, only one newspaper stock, McClatchy, is still worth more today than in January, 2004. Newspaper stocks "had their worst week in memory, despite already low expectations going into the week," said securities analyst John Janedis of Banc of America Securities, adding that missed 2004 sales targets "offset by cost controls were not enough to satisfy [market] concerns of another disappointing year [in 2005]."

So, not only are credibility, circulation and market share crumbling, but stock prices are falling, too. Why?

The market moves for many mysterious reasons, but this one is obvious: Investors, who generally like to bet on the long-term upside of a company, are worried that the publishers don't have a plan for the future of the newspaper business.

While existing shareholders for the moment may be comfortable harvesting the properties for profits, there is not enough new money confident in the long-term prospects for newspapers to lift the value of their stocks.

If newspaper investors want their shares to rise significantly in the future, they are going to have to encourage management to emphasize top-line, not bottom-line, growth. If they don't, they some day will wake up to find the news business has gone the way of the once indomitable Penn Central Railroad.

To change management behavior, the incentives offered to newspaper executives have to reward the development of new products that leverage the existing strengths of their franchises to create sustainable and growing revenues from both existing and new audiences.

Opportunities abound in everything from direct-marketing programs to cellphone text messanging and from targeted, free print editions to paid, premium online content. But newspaper companies won't explore these and many other potentially lucrative paths unless their executives know they can venture outside the box without getting their ears boxed.

The current compensation system not only doesn't encourage change. It all but prohibits it.

posted by Newsosaur at 11:50 PM

![]()

![]()

2 Comments:

Buzz Merritt, former editor of Knight Ridder's Wichita Eagle, has a new book out called "Knightfall" documenting the rise of corporate journalism at papers such as The Philadelphia Inquirer, The Miami Herald, The Detroit Free Press, The Charlotte Observer, and the San Jose Mercury News. There's an excerpt online at Poynter.

Buzz Merritt, former editor of Knight Ridder's Wichita Eagle, has a new book out called "Knightfall" documenting the rise of corporate journalism at papers such as The Philadelphia Inquirer, The Miami Herald, The Detroit Free Press, The Charlotte Observer, and the San Jose Mercury News. There's an excerpt online at Poynter.

Post a Comment

<< Home