More of less

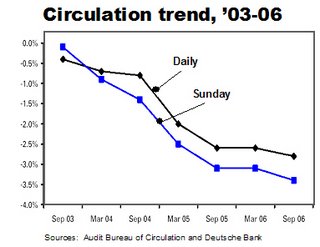

To no one’s surprise, circulation continued sliding at most of the nation’s metro papers over the last six months.

But a significant portion of the decline results directly from the industry’s long-term, and arguably long-overdue, initiative to eliminate inefficient vanity and promotional circulation.

This is not to say that bad circulation is a good thing. Just that it may not be as bad as it seems. One can hope…

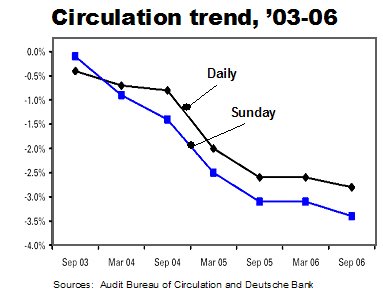

Average circulation in the last six months fell 2.8% daily and 3.4% Sunday, according to an Editor & Publisher analysis based on reports from the Audit Bureau of Circulations, the industry-funded monitoring group.

Some of the drop, doubtless, results from the growing popularity of the digital media. Squeezing lemons into lemonade as fast as it could, the Newspaper Association of America responded to the circulation drop with a study reporting that nearly 57 million Americans visited newspaper websites for an average of 1.37 minutes per day in September.

Notwithstanding the demographic and competitive pressures eroding newspaper readership, a notable, if not precisely quantifiable, portion of the loss results from a strategic restructuring occasioned by the industry’s need to bolster its profitability in the face of weak sales.

To avoid reporting a vertiginous plunge in circulation all at once, most publishers have been whittling away at their non-strategic circulation for the last few years. If and when circulation stabilizes, you will know they have finished their housecleaning. The trimming is taking place in three areas:

:: Vanity circulation – Publishers increasingly are deciding to stop schlepping papers to thinly penetrated locations far from their core markets. Beyond being an expensive indulgence, vanity circulation is little prized by most advertisers. It makes perfect sense to say bye-bye to the boonies.

:: Discount circulation – Although 60% of a typical metro’s circulation consists of loyal subscribers who pay full price, a paper trying to maintain level circulation from year to year is forced to run continuous discount promotions to gain enough “readers” to make up the other 40%. As most advertisers will readily agree, it makes perfect sense for publishers to get off this high-cost, no-win treadmill.

:: Third-party circulation – A few years ago, newspapers got the idea that they could beef up their circulation by getting third parties, like hotels, schools and car dealers, to buy discounted papers that then would then be given to “readers” for free. Given the high cost of producing – and the dubious value of advertising in – giveaway papers, it makes perfect sense for the industry to junk this junk circulation.

With circulation executives exhibiting so much good sense, maybe the news will be better next year. One can hope…

But a significant portion of the decline results directly from the industry’s long-term, and arguably long-overdue, initiative to eliminate inefficient vanity and promotional circulation.

This is not to say that bad circulation is a good thing. Just that it may not be as bad as it seems. One can hope…

Average circulation in the last six months fell 2.8% daily and 3.4% Sunday, according to an Editor & Publisher analysis based on reports from the Audit Bureau of Circulations, the industry-funded monitoring group.

Some of the drop, doubtless, results from the growing popularity of the digital media. Squeezing lemons into lemonade as fast as it could, the Newspaper Association of America responded to the circulation drop with a study reporting that nearly 57 million Americans visited newspaper websites for an average of 1.37 minutes per day in September.

Notwithstanding the demographic and competitive pressures eroding newspaper readership, a notable, if not precisely quantifiable, portion of the loss results from a strategic restructuring occasioned by the industry’s need to bolster its profitability in the face of weak sales.

To avoid reporting a vertiginous plunge in circulation all at once, most publishers have been whittling away at their non-strategic circulation for the last few years. If and when circulation stabilizes, you will know they have finished their housecleaning. The trimming is taking place in three areas:

:: Vanity circulation – Publishers increasingly are deciding to stop schlepping papers to thinly penetrated locations far from their core markets. Beyond being an expensive indulgence, vanity circulation is little prized by most advertisers. It makes perfect sense to say bye-bye to the boonies.

:: Discount circulation – Although 60% of a typical metro’s circulation consists of loyal subscribers who pay full price, a paper trying to maintain level circulation from year to year is forced to run continuous discount promotions to gain enough “readers” to make up the other 40%. As most advertisers will readily agree, it makes perfect sense for publishers to get off this high-cost, no-win treadmill.

:: Third-party circulation – A few years ago, newspapers got the idea that they could beef up their circulation by getting third parties, like hotels, schools and car dealers, to buy discounted papers that then would then be given to “readers” for free. Given the high cost of producing – and the dubious value of advertising in – giveaway papers, it makes perfect sense for the industry to junk this junk circulation.

With circulation executives exhibiting so much good sense, maybe the news will be better next year. One can hope…

posted by Newsosaur at 10:59 AM

![]()

![]()